Written by: | Post Date: 2026/05/12 14:59 pm | Reading Time: 3 min

RBI's Payments Vision 2028, themed "Shaping India’s Payment Frontier," charts a transformative path for digital payments through December 2028, with direct implications for MSMEs facing liquidity and efficiency challenges. Anchored in user empowerment, fraud safeguards, cross-border efficiency, and business ease, its 15 initiatives address MSME pain points like delayed payments and fragmented financing. For India's 63 million MSMEs contributing 30% to GDP, this vision promises faster cash cycles and tech-driven inclusion.

The Origin

India leads globally in real-time payments, processing nearly 50% of worldwide volume, evolving from paper cheques to UPI dominance under successive RBI visions since 2001. Payments Vision 2028 shifts focus from expansion to trust-building and resilience, recognizing digital penetration across segments via RBI's Digital Payments Index. It emphasizes AI-led data approaches, regulatory innovation, and stakeholder collaboration among banks, fintechs, and customers.

Historically, visions progressed from foundational infrastructure (2001-2004: RTGS, CTS) to inclusion (2012-2015: TReDS groundwork) and globalization (2025: 4Es theme). Now, MSMEs benefit from maturing systems tackling B2B frictions, where delayed receivables hinder growth amid a $240 billion credit gap.

Core Pillars for MSMEs

The vision organizes initiatives under inclusivity, safety, efficiency, and stability, directly easing MSME operations.

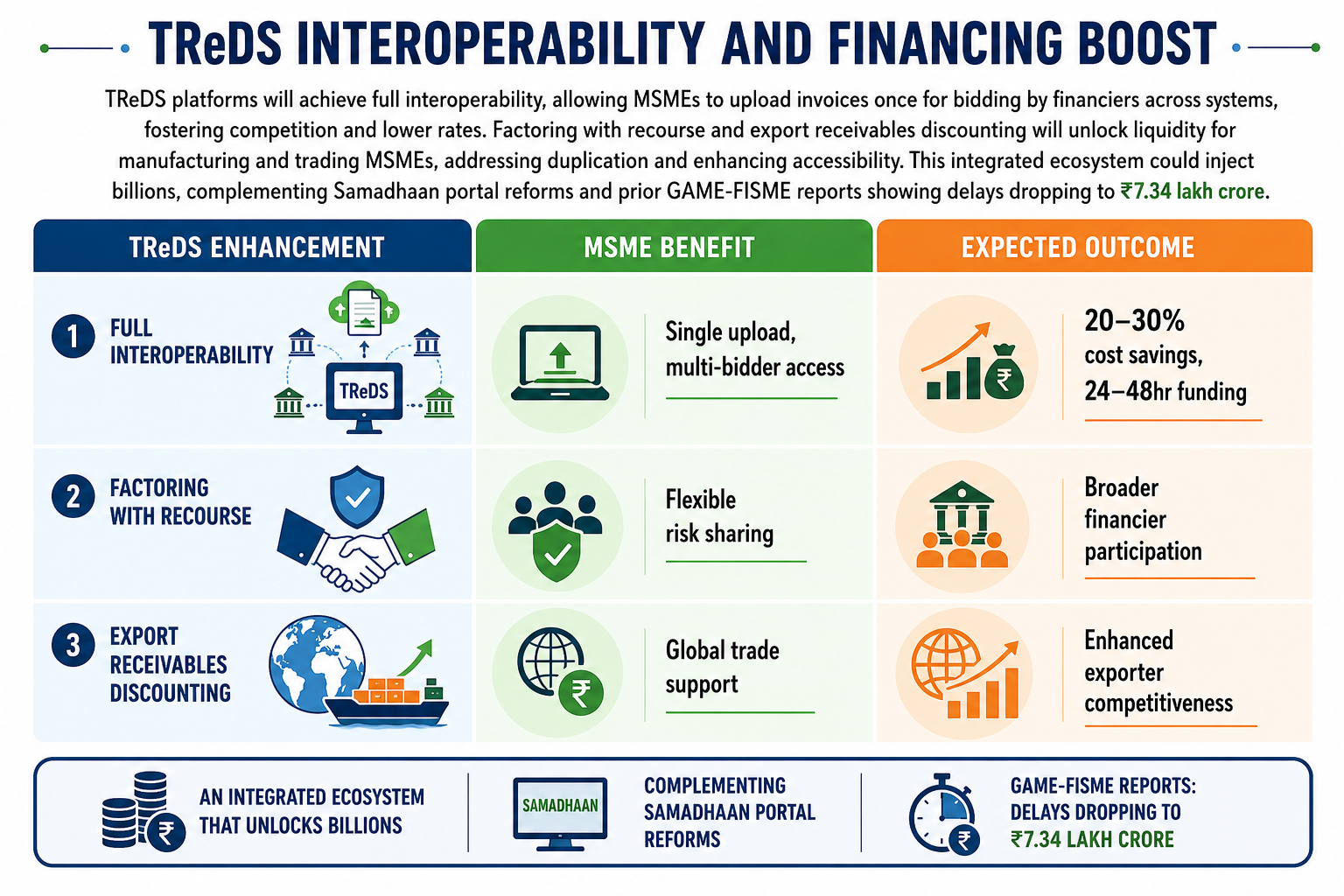

TReDS Interoperability and Financing Boost

Fraud Controls and Transaction Safety

A "switch on/off" facility extends card-like controls to UPI/IMPS, empowering MSMEs to disable modes during risks. Shared liability between issuer and beneficiary banks incentivizes robust fraud detection, reducing chargebacks for small sellers. Cyber Key Risk Indicators (KRI) for non-bank PSOs will monitor resilience, vital as UPI fraud rises.

For D2C brands at events like Bharat D2C Meetups, transactional UPI limits enable safer high-volume payouts.

Cheque Modernization

Cheques persist in B2B MSME payments; a security review standardizes features, curbing fraud variations. Electronic cheques blend paper trust with digital speed, cutting 2-3 day clearances to hours without workflow shifts—ideal for supplier networks.

Cross-Border and Business Efficiency

MSME exporters gain from cross-border framework reviews targeting regulatory frictions, costs, and speed, aligning with G20 goals. Streamlined PSS Act/FEMA authorizations via single-window processes promote innovation. Small Payment System Providers (SPSPs) under perpetual sandboxes lower entry barriers for fintechs serving MSMEs.

Payments Switching Service (PaSS) eases bank switches during mergers, migrating instructions seamlessly. Open card ecosystems and tokenization foster competition, aiding omnichannel D2C scaling.

D2C and Tech Synergies

D2C brands gain from open card ecosystems and Small Finance Banks as PSPs, enabling low-cost UPI/QR scaling for events like Bharat D2C Meetups. AI-powered credit data access complements models sanctioning 98k+ PSB loans, boosting inventory and marketing spends. Cross-border pilots ease exports, aligning with MSME policy pushes at summits.

Challenges and Roadmap

Cyber resilience mandates and AI fraud detection address rising UPI incidents, but MSMEs need upskilling for adoption. Enforcement via Samadhaan enhancements builds on GAME-FISME reports showing delays down to ₹7.34 lakh crore. By 2028, expect 50%+ formalization, fueling Viksit Bharat goals through resilient payments.